Risk Mitigation

July 26, 2024

Overview:

Our team strives to mitigate risk in every step of the predevelopment, construction, and management process to ensure that your investment is safeguarded. During our thorough market research process, we analyze the economic viability, site-specific constraints, and design qualities that will determine the investment feasibility of a project. Next, we research the construction constraints of a site and consider the optimal product for the environment. We constantly update our financial model throughout the underwriting process to maintain our critical financial metrics: Yield On Cost & Internal Rate Of Return. We will start construction once we have finalized the construction drawings, budget, and financial model and close on the financing. We are always trying to optimize our tax strategy through collaboration with BDO and ensure we are leveraging the tax benefits of real estate. Our team partners with Hines to provide best in class institutional quality property management. Finally, we will go to disposition once we have stabilized the project and maximized the sale value. We maintain flexible loan terms to sell an asset at the right time in the economic cycle.

Pre-Development:

Due Diligence:

Our pre-construction due diligence identifies ideal prospective markets and properties while accounting for economic risks. We partner with The Concord Group, which conducts primary market research into the prospective market. They analyze important economic metrics, such as population and job growth, employer-specific changes in the area, rent vs. own trends, local and national affordability factors, absorption studies, and optimize our unit mixes to increase a project’s financial performance. Their industry experience and relationships ensure quality research to help make an educated decision on a project.

Market:

Please see our full market criteria post to see how we create a unique product in growing and prosperous economies based on criteria such as employment and population growth, rental rate, vacancy rate, home affordability, and other factors.

Design:

We utilize design and build contracts with our contractor to decrease variability concerning the cost and timing of a project. Early in the design lifecycle, we set a budget and ensure we design to that budget. Once the budget and guaranteed maximum contracts (GMPs) are executed, financing risks decrease and remain minimal during construction. Change orders are the most significant threat to an increase in costs, which is typical due to unknowns in almost every project. However, that is why we build a design contingency to cover the cost when change orders events occur. Having GMPs contract with our builders ensures that financing requirements and return metrics are accurate and appropriate for the project's scope.

Pre-Construction:

General Contractor Partnership:

We partner with C.D. Smith as our general contractor for our larger projects, including Baker’s Place and The Edison. C.D. Smith is a Wisconsin-based company that embraces the qualities of Midwestern culture and instills them into its professional approach to business. Relationships, trust, and integrity are at the root of its success. Its track record makes it a strong partner in building some of the world’s finest mass timber, Leed Certified, and sustainable buildings. We thoroughly enjoy our partnership with C.D. Smith because they are the only general contractor in Wisconsin and surrounding States that self-perform mass timber erection, which is a massive benefit for us as we only build with mass timber. This significantly reduces the risk of mass timber and, in fact, benefits from using the material because we can accurately predict the construction timeline and erection schedule based on our past experience.

Construction Management:

There are numerous things done to ensure construction quality. First, Neutral is on the site multiple times a week collaborating with the general contractor to ensure project quality. The local municipality also goes to the site weekly, making sure that key deliverables are up to code. C.D. Smith sends out monthly reports on construction progress and things to look forward to, which are forwarded to investors in the quarterly reports.

Guaranteed Maximum Prices:

We utilize Guaranteed Maximum Price (GMP) contracts with our general contractor, C.D. Smith, to alleviate price inflation risk. By the time we break ground, we target 95% of the hard costs to have GMPs. This reduces the likelihood of substantial cost overruns during construction, which can lead to capital calls.

Financing:

Financial Underwriting:

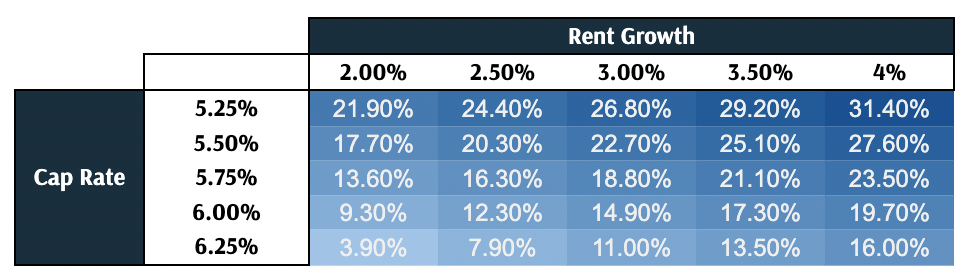

Our underwriting fundamentals don’t let a project proceed without a minimum of a 14% investor internal rate of return (IRR) and 1.75 equity multiple (EMx). We run sensitivity analyses to see how macroeconomic and microeconomic factors affect property performance. Contingency is built into the financial model and thoughtfully analyzed at each point of the development process based on GMPs and progress throughout construction. We also account for a minimum vacancy rate equal to or greater than what is in the local market for the asset class. At an absolute minimum, our financial model must reflect a 5% vacancy rate for lenders to proceed with a project. Lastly, we underwrite a rental growth rate of no greater than 3% per annum, even though we have seen some markets that we develop at 4%-9% year-over-year rental rate escalation in the last few years.

Here is an example sensitivity analysis that compares rent growth and sale cap rate for our project, 519 West Main Street, over a three-year period.

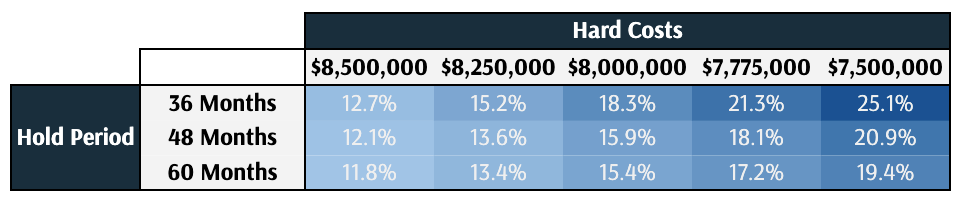

Here is an example sensitivity analysis that compares our project's hard cost and hold period, 519 West Main Street.

Rental Income Growth vs Expense Growth:

Our proformas determine Rental income growth using market data from The Concord Group. Robust economic environments like Madison, WI, with stronger demand side metrics, have high rental growth rates. Rents are also pushed up as consumers rent instead of buy due to the higher interest rate environment. Expense growth is typically not a concern for our properties due to the energy efficiency design we employ and the fact that we usually need to hold projects longer to spend significant capital expenditures. We have repairs and maintenance reserve accounts in our operating expense budget to account for any potential costs that may arise for unforeseen capital expenditures. For conservative underwriting practices, rent and expense growth is at 3% in our financial models.

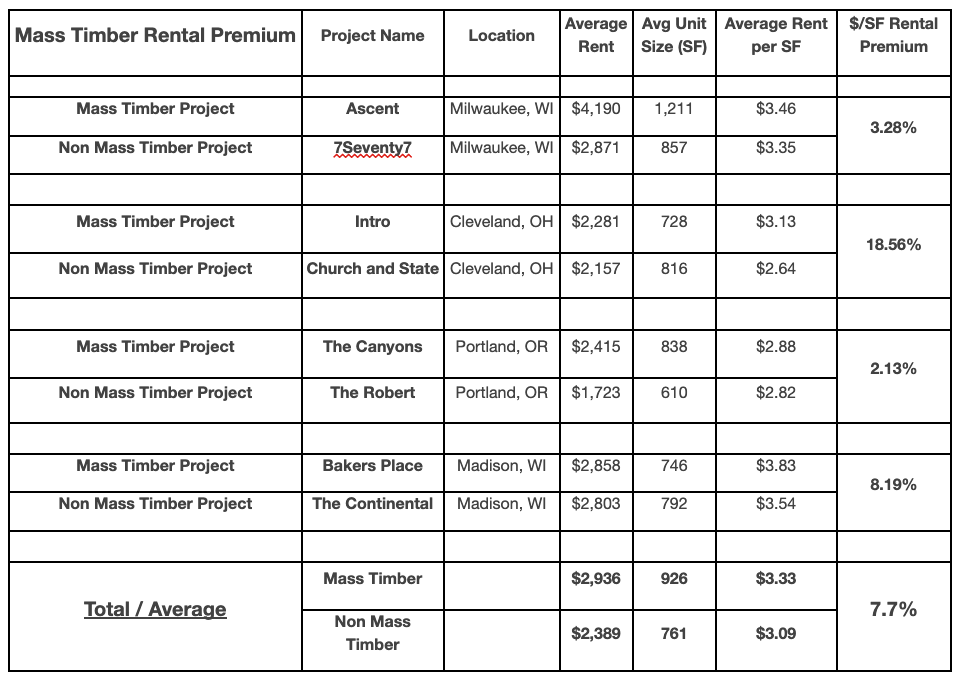

Markup on comparable properties:

Our properties are strictly mass timber, and we have evidence that residents are willing to pay more for this type of project because of its biophilic living experience.

Vacancy Rate:

Vacancy rates are very dependent on the market. We are building a higher quality product that reduces vacancy and collection loss for our properties. However, in specific markets, like Madison, WI, there is such a low vacancy rate that the vacancy rate in our proforma is higher than the marketplace average. Our lenders require that we maintain a minimum of a 5% vacancy rate. We use these rates in our financial model to project returns.

Risk Adjusted Returns:

Risk-adjusted returns compare an asset’s performance to the “risk-free rate.” The risk-free rate is tied to government bonds, as they are perceived as “riskless” from an investor's point of view. While US government bonds are among the highest-graded bonds in the world, they were recently downgraded to “AA+” from “AAA” due to debt limit standoffs and last-second resolutions, along with rising government deficits driven by high government spending (Fitch Ratings 2023).

An asset’s expected return is projected using the Capital Asset Pricing Model, or CAPM. The formula is E(Ri) = Rf + βi(ERm - Rf). The Expected Return of an Asset equals The Risk-Free Rate plus An Asset’s Beta times the difference between The Expected Return of The Market and The Risk-Free Rate. The critical factor here is an asset’s beta, which determines the severity of an asset’s change in price relative to the market. Assets with a beta greater than 1 are considered more volatile than the market, and assets with a beta less than 1 are considered less volatile. While the CAPM is beneficial, “the CAPM was only able to explain about two-thirds of the differences in returns of diversified portfolios” (Berkin, Swedroe, 2016).

As commonly known, investors should have a diversified portfolio. While investors would like to hold assets that will increase their portfolio's expected return, it is important to account for the standard deviation of returns and keep their risk appropriate. Holding assets that have negative correlations to each other keeps the standard deviation (variability) of the expected returns minimal while keeping the overall expected return of the portfolio high.

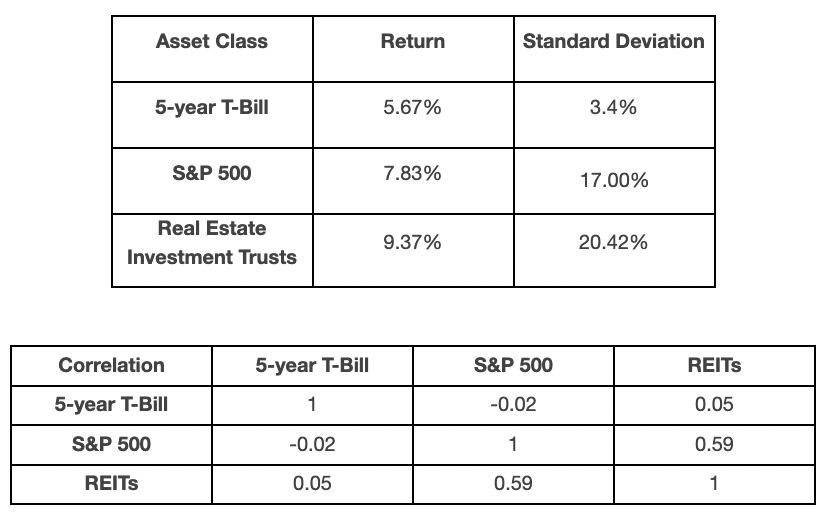

The summary below compares historical returns of 5-year treasury bills, the S&P 500, and REITs from 1972-2023. Some of the key takeaways from the analysis show that the average return and standard deviation below:

The standard deviation for 5-Y T-Bills was significantly less than that of the S&P 500 and REITS, at 3.4% for T-Bills, 17% for the S&P 500, and 20.42% for REITs. One standard deviation accounts for 68% of values, 34% on either side of the mean. So for REITS with an average return of 9.37%, 68% of returns were between -11% and 30%. The T-Bills had the lowest volatility and lowest returns. REITs had the highest volatility and highest returns. The S&P 500 and REITs had a correlation of 0.59, which is considered a moderate to strong relationship. Lastly, 72.5% of the time, the S&P 500 and REITs experienced both positive or negative returns.

This correlation suggests that for a portfolio to be well diversified if it is only diversified between stocks and bonds, the portfolio allocation that should go to Real Estate should be taken out of stocks.

Construction:

Interest Rate Hedging:

We use JLL and its derivatives arm, Kensington Capital Advisors, to help us hedge our interest rate risk during construction. Our construction loans are based on a variable debt rate; this means that the loan is floating at a rate typically around 3% to 4% over the Secured Overnight Financing Rate (SOFR) for the senior loan position and 7% to 9% over SOFR for the mezzanine position. To hedge the risk of the floating nature of the loan, we purchase a SOFR cap to lock in our SOFR rate, typically at 2.5% to 4%. Therefore, the all-in rate on senior loans is generally at 5.5% to 8%, and for mezzanine loans, it is at 9.5% to 13%. To learn more about SOFR caps and other derivatives we use, please watch the video at the top of the page. JLL is also our debt broker, which allows us to work with them on all steps of the debt solicitation process. JLL is a Fortune 500 company with operations in over 80 countries with 108,000 employees. Their expertise in various topics makes them a great partner in securing financing.

Sustainable Material:

Mass timber projects allow faster construction schedules than its counterparts, such as steel and concrete, which helps meet scheduling goals. Quality relationships with the general contractor ensure that all aspects of the project are fulfilled. Furthermore, C.D. Smith, the general contractor on our large projects and a super subcontractor on our smaller developments, self-perform the mass timber erection, and have become the experts in the Midwest of mass timber construction.

Long Term Efficiency:

Our design and construction process aims for sustainability certifications while also working with the local government to identify suitable designs for each environment. Passive House qualities reduce the ecological footprint of the building through lower energy consumption for heating and cooling. Our developments are also LEED (Leadership in Energy and Environmental Design) Certified which provides a framework for healthy, highly efficient, and cost-saving green buildings.

Inflation and Market Correlation

Real estate, particularly multifamily real estate, often exhibits a low or negative correlation with traditional asset classes like stocks and bonds, making it resilient when the stock market becomes bearish. This non-correlation can help balance total investment returns when public markets underperform. Additionally, multifamily real estate serves as an effective inflation hedge, as it tends to keep pace with or even outpace inflation. Residential rental income and property values can rise alongside the cost of living, preserving purchasing power over time. Unlike other real estate asset classes, such as office space, multifamily properties benefit from annual lease renewals that adjust rental rates to mirror inflation. For instance, during the unprecedented inflation of 17.7% from 2021 to 2023, multifamily rents in Madison, WI, rose by 30.4% (Srinivasan 2024; Reynaga 2023), highlighting the sector's ability to hedge against inflation. Furthermore, development real estate projects offer opportunities for long-term appreciation. Stabilized real estate properties are sought after by institutional investors, private equity firms, family offices, REITs, sovereign wealth funds, pension funds, high-net-worth individuals, and real estate funds for their consistent income, leveraging potential, and tax benefits.

Tax:

Tax opportunities:

Sustainable development offers tax opportunities to developers and investors thanks to the 2022 Inflation Reduction Act. Dollar for dollar tax credits are sought during the year after the building is placed in service. These tax credits and tax deductions will decrease an investor’s taxable income, reducing their total tax liability. Please see our full tax post to see the numerous tax benefits available with Real Estate Investing.

Tax Abatement:

TIF, or Tax Incremental Financing, is a public financing method to help developments, ultimately reducing the costs of projects. Implementation of beneficial projects in communities creates a strong argument for city governments to award TIF, and has already been used for Neutral’s development, The Edison.

Property Management:

We outsource property management to Hines and their property management arm, Willowick Residential, to maximize the cash flow of a property before disposition. Hines’ success and reputation as a property management company draws future buyers at the end of our ownership to ensure the success during the entire period between pre-lease up to sale. Hines has almost 70 years of experience with more than $93 billion in assets under management, and has a strong reputation for their success in providing luxury property management services.

Disposition:

Our sale cap rates are determined given the nature of the property, location, and comparable sales in the area. Additionally, cap rates tend to move with interest rates, so when interest rates go up, so do cap rates and vice versa. Our exit cap rates are forecasted considering changes in interest rates, which are determined from information we receive from Kensington Capital on the forward interest rate curves.

Works Cited

Berkin, Andrew L., and Larry E. Swedroe. Your Complete Guide to Factor-Based Investing. BAM Alliance Press, 2016.

Fitch Ratings "Fitch Downgrades United States' Long-Term Ratings to 'AA+' from 'AAA'; Outlook Stable." Fitch Ratings, 1 Aug. 2023, www.fitchratings.com/research/sovereigns/fitch-downgrades-united-states-long-term-ratings-to-aa-from-aaa-outlook-stable-01-08-2023.

Reynaga, Jenny. “Madison Year-over-Year Rents Rose Highest in the Nation, Study Finds.” Madison Year-over-Year Rents Rose Highest in the Nation, Study Finds - The Daily Cardinal, 5 Apr. 2023, www.dailycardinal.com/article/2023/04/madison-year-over-year-rents-rose-highest-in-the-nation-study-finds#:~:text=As%20of%20March%202023%2C%20a,an%20average%20rate%20of%201.1%25.

Srinivasan, Hiranmayi. “U.S. Inflation Rate by Year: 1929 to 2024.” Investopedia, Investopedia, 31 July 2024, www.investopedia.com/inflation-rate-by-year-7253832#:~:text=In%202023%2C%20the%20average%20rate,of%20inflation%20was%201.2%25.7.